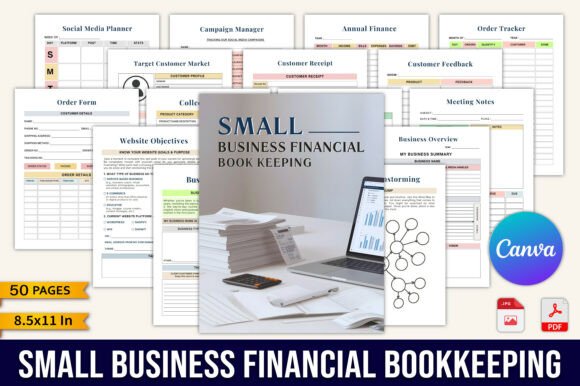

Small Business Financial Bookkeeping: Clarity, Control, and Consistency for Growing Businesses

Small Business Financial Bookkeeping is more than recording income and expenses—it’s the ongoing practice of organizing, categorizing, and interpreting financial data to support sound decision-making. Unlike personal finance tracking or enterprise-level accounting systems, Small Business Financial Bookkeeping bridges simplicity and structure: it’s designed for founders who need accuracy without complexity, consistency without bureaucracy, and insight without dependency on a CPA for day-to-day operations.

At its core, this practice involves regular documentation of transactions, reconciliation of accounts, classification of spending (e.g., supplies vs. marketing vs. home office), and alignment with tax obligations. What makes it distinct isn’t just the tasks involved—but how those tasks are contextualized within the rhythm of running a small business: seasonal demand shifts, irregular cash flow, evolving service offerings, and the constant interplay between time, revenue, and overhead.

How It Fits Into Broader Business Management

Many entrepreneurs mistakenly treat bookkeeping as a standalone administrative chore—something to “get done” quarterly or before tax season. In reality, effective Small Business Financial Bookkeeping serves as the backbone for planning, pricing, hiring, and even customer communication. When your expense tracker reflects actual ad spend per campaign, your sales tracker shows which product variants drive repeat purchases, and your tax deduction log captures mileage and software subscriptions in real time, you’re not just preparing for taxes—you’re building operational intelligence.

This is where tools like The Small Business Financial Bookkeeping Planner become practical: they embed bookkeeping habits into broader business routines. Rather than toggling between spreadsheets, calendars, and notes apps, users maintain continuity across daily scheduling, order fulfillment, content planning, and financial review—all in one physical or printable format. The planner doesn’t replace accounting software, but it complements it by capturing context that software often misses: why a certain expense was incurred, how a promotion performed against expectations, or what customer feedback preceded a pricing adjustment.

Strengths: Where This Approach Excels

Small Business Financial Bookkeeping shines when clarity and consistency matter more than automation. For solopreneurs, micro-businesses, and early-stage ventures, its strengths include:

- Low technical barrier: No learning curve tied to cloud platforms, bank feeds, or chart-of-accounts setup.

- Context-rich documentation: Notes beside an expense entry (“Client meeting prep—printed samples + coffee”) support later tax justification and internal review.

- Integrated planning: Linking budget goals to monthly sales targets, then to seasonal promotions and social media activity, reveals cause-and-effect relationships software alone can’t surface.

- Ownership and awareness: Writing down numbers—and reflecting on them weekly—builds financial literacy faster than passive dashboard scanning.

Consider a handmade jewelry seller launching her first holiday collection. Using the planner’s Order Tracker, Seasonal Promotions, and Expense Tracker side-by-side, she notices that Instagram ads drove 60% of pre-orders—but packaging costs rose 25% due to custom boxes. That observation informs next year’s margin calculations *before* she finalizes vendor contracts.

Tradeoffs and Realistic Limitations

No approach is universally optimal. Small Business Financial Bookkeeping—especially in planner-based form—has clear tradeoffs:

- No automatic bank reconciliation: Manual entry means time investment and risk of human error. If you process 50+ transactions weekly or accept payments across multiple platforms (Etsy, PayPal, Square), spreadsheet or app-based tracking may reduce friction.

- Less scalable for teams: Shared digital files allow real-time collaboration; physical planners require coordination, scanning, or duplication—making delegation harder as staff grows.

- Limited reporting depth: While the planner includes sections like Annual Profit & Loss and Monthly Sales, it doesn’t auto-generate charts, trend lines, or comparative YOY analysis. Users must interpret patterns themselves—or export data elsewhere.

- Dependence on discipline: Its value hinges on consistent use. A planner left unopened for three weeks creates gaps that compound—not just financially, but cognitively (e.g., forgetting deductible expenses or misattributing revenue sources).

That said, these aren’t flaws—they’re design choices aligned with specific needs. A freelance graphic designer billing 8–12 clients monthly may find the planner’s Invoice Log, Customer Receipt, and Income Tracker perfectly matched to her workflow. A local bakery managing payroll, inventory, and wholesale invoices likely needs integrated point-of-sale and accounting software instead.

When to Choose This Approach—and When to Look Elsewhere

Small Business Financial Bookkeeping using a structured planner works best when:

- You’re operating solo or with 1–2 team members.

- Your revenue is under $100,000 annually—or highly variable (e.g., project-based, seasonal, or service-led).

- You prefer tactile, reflective work over digital dashboards.

- You want to build foundational habits *before* adopting complex tools.

- Your primary pain point is disorganization—not data volume or compliance complexity.

It becomes less ideal when:

- You regularly reconcile dozens of bank and credit card accounts.

- You issue recurring invoices, manage inventory SKUs, or track job costing.

- You need audit-ready records with version history, permissions, or third-party integrations (e.g., QuickBooks + Shopify sync).

- You’re required to file VAT/GST, payroll taxes, or multi-state sales tax routinely.

Importantly, these aren’t mutually exclusive paths. Many businesses start with a planner to establish rhythm and categories, then migrate key functions to software once volume or regulation demands it. Others use the planner alongside digital tools—as a “thinking layer” for strategy and reflection, while software handles transactional accuracy.

Practical Integration Tips

If you’re evaluating whether Small Business Financial Bookkeeping fits your current stage, consider how it would integrate—not replace—your existing systems:

- Start with one section: Try the Budget Tracker alongside your current expense app for one month. Compare entries manually—does it surface overlooked categories (e.g., subscription renewals, professional development)?

- Test cross-reference points: Use the Sales Tracker to log each invoice, then compare totals to your payment processor at month-end. Discrepancies highlight timing differences (e.g., pending payouts) or missed entries.

- Review with purpose: Block 30 minutes weekly—not just to fill in blanks, but to ask: What surprised me? What repeated? What do I need to adjust next week?

- Keep receipts intentionally: Use the Tax Deduction page not as a dump, but as a filter: Does this qualify? Is it documented? Can I explain it simply if asked?

Over time, this builds what many small business owners lack—not just numbers, but narrative. You begin to see how a slow March impacts Q2 goal pacing, how customer feedback in the Feedback section aligns with spikes in Support Time logged in Weekly To Do, or how last year’s Seasonal Promotion plan informs this year’s Marketing Plan.

Making an Informed Choice

There’s no universal “best” method for Small Business Financial Bookkeeping—only what fits your capacity, goals, and growth trajectory. Planners offer structure without infrastructure; software offers power without presence. Some entrepreneurs thrive with hybrid approaches: logging daily transactions in an app, then summarizing insights and action items in a planner each Sunday. Others find the physical act of writing reinforces accountability in ways digital alerts cannot.

What matters most is consistency, relevance, and intentionality. Whether you choose a dedicated planner, a customized spreadsheet, or a cloud-based platform, prioritize tools that encourage regular engagement—not just data capture. Because Small Business Financial Bookkeeping isn’t about perfection. It’s about showing up, staying aware, and making decisions grounded in reality—not hope.